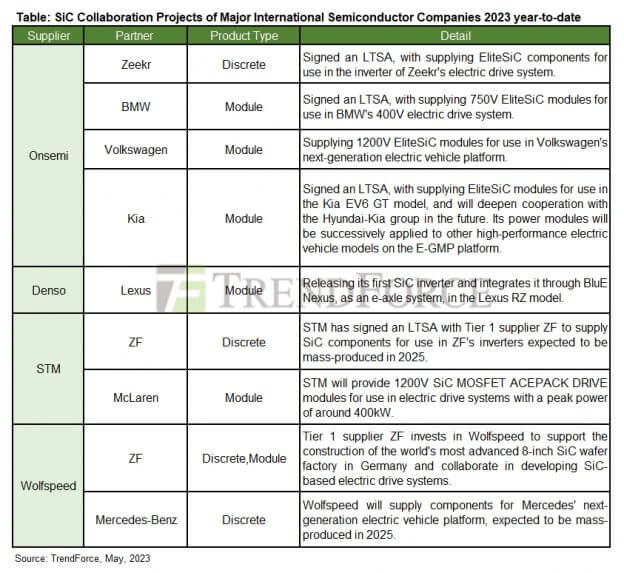

Onsemi, a semiconductor manufacturer, announced at the end of April that it had signed a Long-Term Supply Agreement for SiC power components with Zeekr, a subsidiary of Geely Auto Group. Geely Automotive will use Onsemi’s EliteSiC power components to optimize energy conversion efficiency in its electric drive system. This move signals Onsemi’s aggressive expansion in the automotive SiC market, catching up to leading manufacturers STMicroelectronics and Infineon.

In the SiC semiconductor market for electric vehicles, STMicroelectronics and Infineon have maintained their market leadership by entering the market early, while Wolfspeed and ROHM have gained traction through their vertical integration technology for SiC. On the other hand, Onsemi still lags behind in terms of market share for SiC power semiconductors, even though it acquired GT Advanced Technologies in 2021 and mastered the most difficult wafer growth and production equipment technology in SiC manufacturing. Before 2023, Onsemi was only used in small and medium-sized vehicle models such as NIO and Lucid.

However, Onsemi’s benefits begin to materialize in 2023, thanks to the industry maturity built by early players such as Infineon and STM, combined with Onsemi’s early deployment of SiC-related technology. Onsemi’s SiC product EliteSiC has obtained LTSA from Zeekr, BMW, Hyundai and Volkswagen in the form of discrete and modules. Its CEO, Hassane El-Khoury, has stated that the SiC business will generate $4 billion in revenue over the next three years compared to the total revenue for the 2022 SiC market of approximately $1.1 billion. These factors have made Onsemi the most talked-about semiconductor company in the SiC market this year.

However, the intense competition in the SiC market will test the endurance of resource input sustainability. The rapid growth in SiC demand over the past five years is mainly due to high battery costs and the development of energy density having reached its limit. Car manufacturers have switched to using SiC chips in their electronic components to increase driving range without increasing the number of batteries.

As a result, car manufacturers are aggressively pushing semiconductor companies to accelerate their research and development of SiC technology. This has resulted in a significant reduction in R&D time, but also an increase in R&D costs. Coupled with the impact of intense market competition on profits, the ability to sustain R&D resource input and overall profitability performance will be the key indicators of semiconductor companies’ competitiveness.

Onsemi has successfully improved its profitability performance by streamlining its product lines over the past few years, ranking at the top with a 49% gross margin, according to the financial reports of various semiconductor companies in 2022. This profitability performance allows Onsemi to meet car manufacturers’ cost requirements and secure orders, thereby achieving economies of scale in SiC product growth.

However, in terms of R&D costs as a percentage of revenue, Onsemi ranks last at 7%, compared to its main competitors Wolfspeed (26%), Infineon (13%), STM (12%), and ROHM (8%). With semiconductor companies investing more in technologies such as reducing on-resistance and improving yield rates, how to maintain a balance between profitability performance and resource expenditure while achieving revenue goals through intense market competition will be an important challenge for Onsemi after securing orders from car manufacturers.

{kind=link}