Tesla’s next-generation EVs may feature a novel packaging design for the primary inverter, utilizing a hybrid SiC/Si IGBT packaging approach.

The SiC market has been very active lately, with constant news coming from device suppliers and car makers. And there seems to be an ongoing tug-of-war between supply and demand.

Toshiba announced in April the groundbreaking of its power semiconductor fab for SiC in Ishikawa Prefecture, with the first stage beginning in the 2024 fiscal year. This news echoes earlier reports from Japanese media that Toshiba is strengthening the vertical integration throughout SiC equipment, wafers, and devices, and planning to increase the production by three times in 2024 and 10 times by 2026.

Meanwhile, over the past two years, leading companies in the Europe and the US such as Infineon and ST have also accelerated M&A as well as internal expansion for SiC production devices at an unprecedented pace, aiming to expand their SiC-related businesses and maintain their core competitiveness in the market.

Despite aggressive demand-driven expansion plans, the unexpected announcement from Tesla in mid-March that it plans to reduce overall SiC usage by 75% in the next generation of electric vehicle platforms has sparked various speculations in the industry. This move was made without compromising the performance and efficiency of the cars and represents one of the few specific details that Tesla has revealed about its new car plans.

Now here is the question – will the popularity of SiC be a genuine trend, or merely a passing fad that could lead to a potential bubble in the market?

SiC or Si-based solutions?

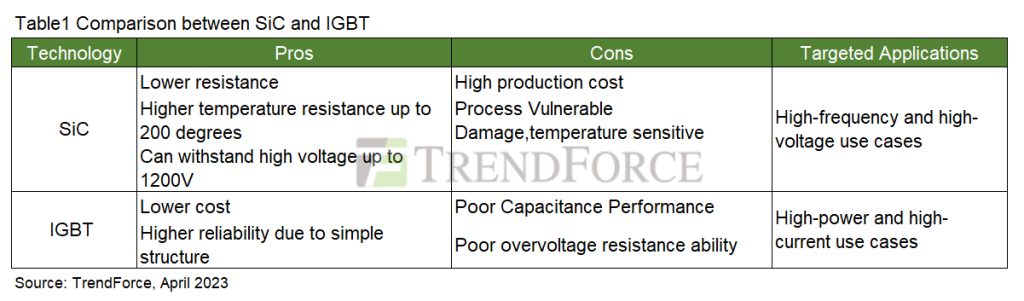

Compared to IGBT and MOSFET, the dominant technologies in power semiconductor, SiC offers stronger advantages such as low resistance, high temperature and high voltage tolerance that can overcome the technical bottlenecks of EVs by improving battery efficiency and solving component heat dissipation issues. SiC can also make chip design sizes smaller, which means more flexibility in vehicle design.

These advantages have made SiC the most sought-after technology. According to TrendForce, the SiC power device market is expected to grow at a CAGR of 35% to reach $5.33 billion annually from 2022 to 2026, driven by mainstream applications such as electric vehicles and renewable energy.

There is a long-standing debate among the industry about whether SiC will replace IGBTs entirely. What we believe is that SiC may not completely replace IGBTs considering their distinct targeted use scenarios.

In terms of use cases, SiC is particularly suitable for high-frequency, high-voltage applications, especially in the field of new energy vehicles. Traditional Si-based IGBT chips have reached the physical limit in high-voltage fast charging models, making SiC more favorable for new energy vehicles.

However, SiC transistors are expensive due to complex production processes, slow crystal growth, and difficult cutting. Unlike silicon, which can be pulled quickly, SiC crystals grow at a slow rate of 0.2-1mm/hour and are prone to cracking during the cutting process due to their high hardness and brittleness, leading to hundreds of hours of cutting time.

Additionally, SiC transistors also have some drawbacks such as vulnerability to damage and temperature sensitivity, which makes them unsuitable for low-cost and low-power applications.

IGBT, on the contrary, is preferred over SiC in such a field because it is more cost-effective, reliable, and has better capacitance and surge capability for high-power and high-current applications. In certain scenarios, such as DC-DC charging piles, IGBT is irreplaceable due to its cost advantage and suitability.

Could a Hybrid Solution be the Answer?

The premise above can help to explain Tesla’s conflicting decision to cut back on SiC usage.

Tesla’s reluctance to fully adopt SiC technology is mainly due to concerns about reliability and supply chain stability, as evidenced by a mass recall of Model 3 due to issues with SiC components in the rear electric motor inverter.

In addition, the shortage of substrate materials is another challenge facing the SiC industry as a whole, with major manufacturers such as Wolfspeed, Infineon, and ST ramping up production capacity to address the issue. As a result, Tesla is considering alternative ways to mitigate the risks associated with supply chain constraints.

Despite these challenges, SiC remains a promising trend for the EV industry. Even Tesla recognizes its enormous potential commercial value.

In terms of technological innovations, Tesla’s next-generation EVs may feature a novel packaging design for the primary inverter, utilizing a hybrid SiC/Si IGBT packaging approach that leverages the unique strengths of both technologies while avoiding potential pitfalls. This technological advancement poses certain difficulties, but the groundbreaking innovation at the engineering design level is definitely something to look forward to.

{kind=link}