The rapid growth of the new energy vehicle industry has put China on the edge of a new technological revolution.

What does this mean for investors? What trends are coming for the sector? Analysts at TF Securities expressed their views and gave their ten predictions in a lengthy report released on Tuesday.

They believe that smart cars are expected to become the world’s biggest entrepreneurial opportunity after the Internet, and will start a new wave of fortune creation.

China, one of the world’s largest smart car markets, is fully embracing the trend of smart transformation and the country will become the world’s smart car hub, they argue.

In this trend, joint venture brands in China that are slow to transform may lag behind and local brands will have the opportunity to overtake.

The eventual winners in this market will include traditional car companies that are transforming quickly, leading new car makers, and some technology companies that are actively participating.

Here are the key takeaways from their report, compiled by CnEVPost.

Prediction 1: Smart cars are expected to become the world’s largest entrepreneurial opportunity after the Internet

The Internet was born in California in 1969, and in the following decades, the development of the Internet has brought huge business value and investment opportunities.

Smart cars will take over the Internet in the future, opening up the wealth creation effect, and many companies are already involved in it.

Global smart car market shipments will reach 76.2 million units in 2024, with a compound annual growth rate (CAGR) of 16.8 percent from 2020 to 2024, according to the IDC Global Smart Connected Vehicle Forecast Report.

China, one of the world’s largest smart car markets, is fully embracing the trend of intelligent transformation, and the industry has received strong support at the national level.

China is the world’s number one auto consumer market with the fastest technological change. 2020, global auto sales will total 78.03 million units, with China’s auto sales at 25.27 million units, reigning as the world’s number one, accounting for 32 percent of the global share.

China’s smart car industry is large in scale, fast in growth, and increasing in penetration rate.

The scale of China’s smart connected car industry will grow to RMB 255.6 billion in 2020 and is expected to reach RMB 585.9 billion in 2026, with a CAGR of 14.8 percent.

According to the National Development and Reform Commission forecast, the number of smart cars in China will reach 28 million in 2025, with a penetration rate of 82 percent. By 2030, the number will reach about 38 million units, with a penetration rate of 95 percent.

With vehicle manufacturing as the core, there are plenty of innovation opportunities for smart vehicles.

Among them, upstream companies include perception, control, and communication system manufacturing industries, with major products including chips, radar, and maps. The midstream companies include the executive system manufacturing industry with major products including intelligent center control screens. The downstream is mainly the service industry of development, testing, and operation.

Traditional car companies, car-making new forces, and technology giants invest heavily in car-making, the synergistic development of smart cities, smart cars, smart travel, and smart transportation has become an inevitable demand.

The core technology of smart cars cannot be separated from the development of AI, big data, cloud computing, and systems. This will be the main direction for the transformation of traditional auto giants, and also the entry point for new car-making forces and technology giant companies to enter the car-making track.

The declining cost of building cars and the changes brought by business models provide opportunities for startups, and all companies are basically at the same starting line when they enter.

The core components of fuel cars are the engine and transmission system, accounting for 25 percent of the total cost of the vehicle. The core components of new energy vehicles are batteries, electric control, and motors, accounting for more than 50 percent of the cost. Future electronic components in the car cost ratio will continue to rapidly increase to about 50 percent or more.

The automobile will be the largest market in terms of volume and change after the smartphone. Intelligence has become a key driving factor for the technology giants to come down to the field.

After the “software-defined car” has become the consensus view, the imagination brought by the software is more compelling.

Prediction 2: China will become the world’s smart car hub

China has the advantage of information and communications technology (ICT) technology, which is the foundation for smart cars.

In 2020, China’s ICT technology maturity curve covers 24 technologies and practices. The exponential growth of Internet users over the past few years has accelerated the digital transformation by various technology companies launching their own data hubs.

The strong ICT technology accumulation represented by Huawei has laid a solid foundation for the pioneering of China’s smart driving sector.

According to the data of the US Bureau of Economic Analysis on the labor participation rate of countries in the world, China is the first in the world in terms of total labor volume and the first in the world in terms of the labor participation rate.

At the start-up stage of smart cars, Chinese diligence will accelerate China’s smart car technology breakthrough.

The US led the world in self-driving funding in 2019 with $4.5 billion in funding, followed by China with $2.3 billion. Combined, the US and China bagged 94 percent of the global funding total.

Autonomous driving is one of the most promising areas among the many commercial targets of artificial intelligence and thus is the area with the earliest layout time and many layout companies.

In addition to traditional vehicle and component companies, technology-based companies, including Huawei, Baidu, Alibaba, Tencent, and DJI Technology, are also accelerating their presence in China.

China has become the country with the largest number of patents in the field of smart vehicles.

In 2017, there were 32,000 smart car-related cases worldwide, with China accounting for 37 percent, followed by Japan, the United States, Germany and South Korea with 20 percent, 16 percent, 12 percent and 7 percent respectively. The combined share of these five countries is close to 95 percent.

Benefiting from the government’s policy support for patent applications, Chinese companies have surpassed Western countries in the number of patent applications in the field of smart connected vehicles.

In 2020, the number of smart cars on the market in China will account for 34 percent of the total number of cars. Among them, the smart cockpit is equipped with 86 percent, smart driving with 68 percent, and OTA with 43 percent.

Prediction 3: Local Chinese brands are expected to beat JV brands at home and start to enter the global market

In recent years, sales of French, Italian and Korean joint venture brands in China have been sluggish and on a downward trend, with Opel and Suzuki exiting the Chinese market one after another.

The rapid progress in technology accumulation of local car companies is one of the reasons for this phenomenon. As the aura of joint venture brands slowly fades, local brands still have more room to improve their market share.

In recent years, China’s auto industry has developed rapidly, and local brands have gradually overtaken international brands in the fierce competition in the global auto market.

The “Generation Z”, born between 1995 and 2009, has become the main consumer group, and new cars of local brands with rich technology are expected to gain the recognition of the young people of Generation Z.

In 2020, China will continue to be the world’s number one in auto sales, with a 32 percent share of the global market. 2020 will see China’s economy recover faster, with auto sales narrowing to less than 2 percent year-on-year, and annual sales reigning as the world’s number one, with a 32 percent share of the global auto market.

In recent years, local brands such as Hong qi and Lynk & Co are already trying to enter the high-end market and are going global.

With technological advances, new product launches, and the retreat of joint venture brands, local Chinese brands are expected to reach a domestic market share of more than 70 percent by 2030, with prices per vehicle expected to double and open up the battle for the global market.

Prediction 4: With many market segments, the industry will be able to accommodate more than 10 local car companies

In terms of intelligent assisted travel, improving user efficiency and convenience is fundamental.

The intelligent cockpit will meet the services related to travel and location, so that the user search or even before the demand is raised, to meet the search for nearby clothing, food, housing and transportation, and other scenarios.

Existing vehicle functions will be more intelligent, the image will be clearer, and navigation will be automatically updated in real-time networking.

Vehicle digitalization, online service function of the extension of the Shen will be realized with the application of 5G. In the context of the Internet of everything, multi-device interconnection, online payment in the car and other functions make it more convenient and efficient to use the car.

An intelligent cockpit will enrich the social functions in the car, including ticketing, seat selection, hotel booking, route planning, car dating and other aspects to achieve accurate services.

Intelligent cockpit first of all needs to meet the user’s real-time requirements, to support the user’s office on the road. Entertainment features are relatively secondary and audio-based.

The car market is large enough, personalized needs and a large number of innovations emerge so that many car companies have room to survive, traditional local car companies and car-making new forces have opportunities.

The hardware side of the chip as the core, Horizon Robotics, and Hisilicon has entered the AI chip production.

In terms of software, NIO has launched its voice assistant NOMI, XPeng Motors has launched its intelligent cockpit, and Li Auto has made intelligent cockpit one of its core selling points.

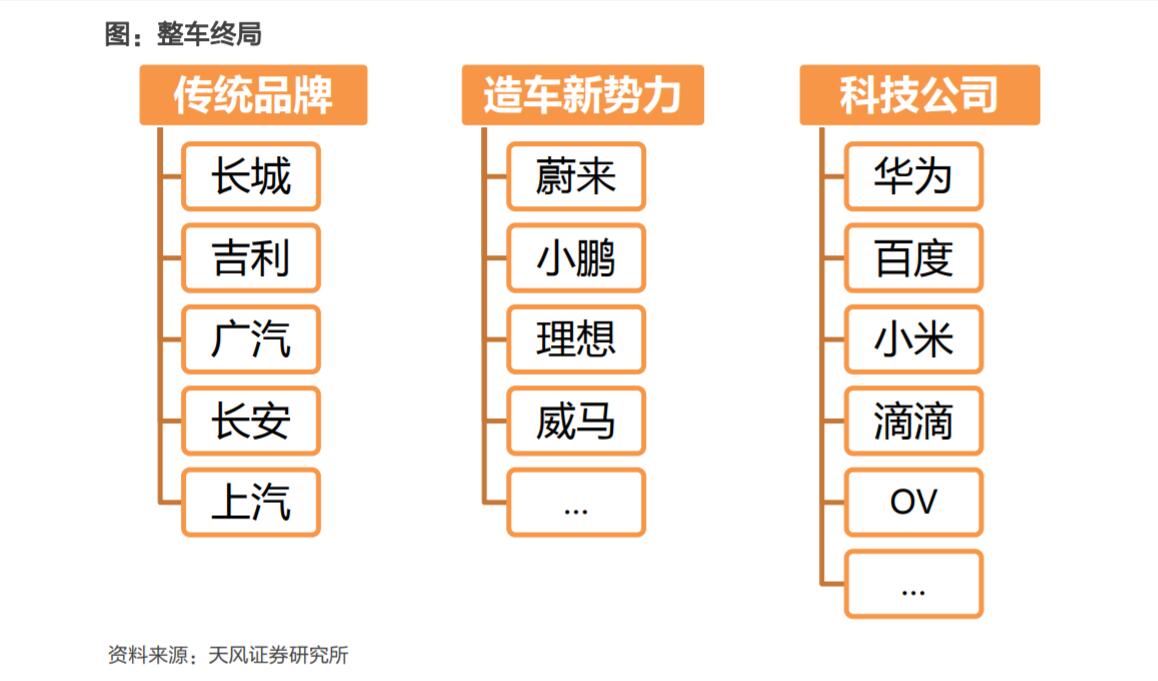

Prediction 5: The endgame of car company competition

With the accumulation of technology and the increase of market concentration, the pattern of car companies will eventually form a “3+3+3” situation, with 3 traditional brands, 3 new power companies and 3 technology companies leading the industry.

The traditional local companies include Great Wall Motors, Geely, SAIC Motors, the new car makers include NIO, Li Auto, XPeng, and the technology companies include Huawei, Baidu and Xiaomi.

Entrepreneurship is the core resource of a company and one of the requirements for an endgame winner.

Supply chain integration capability is the core competency of the endgame winner of the car company competition. Excellent supply chain integration ability is the most important one and one of the criteria that can guarantee to stand out and be able to enter the endgame.

Full-stack software and hardware R&D and operation development capability is one of the goals pursued by car companies, Huawei already has full-stack R&D strength, and new power car companies and local car companies are also striving to become the Xiaomi ,OPPO and Vivo in the automotive industry.

Prediction 6: Car companies still have more room for growth in market value

There are fewer listed companies in the field of chips and algorithms, and vehicle companies are the most core underlying assets that investors can buy.

Among the listed companies in vehicle manufacturing, BAIC Motor, JAC Group, Great Wall Motors, Changan Motor and SAIC Motors have layouts in both domestic and international markets.

The new vehicle manufacturing forces represented by NIO, XPeng and Li Auto also have vehicle manufacturing capabilities.

Manufacturing and supply chain management capabilities are the core of traditional automotive manufacturing. There are still many shortcomings in the development of China’s auto parts industry, and there are many shortcomings in the upstream and downstream of the industry chain.

For a long time, the overall level of China’s manufacturing industry has hovered in the middle and low end, especially in the segments of industrial special materials, industrial software and control systems, special production equipment and testing systems.

Technology capability is the core of car-making in the new era, and Great Wall Motors, Geely and JAC Group have released new strategies and technologies to accelerate into the new era with technology-driven innovation and head-to-head technology showdown with world brands.

The market value of Tesla and the new car makers has been rising, especially Tesla has far surpassed the traditional auto giants.

As of June 21, 2021, Tesla’s market capitalization has $598.1 billion, more than twice that of Toyota.

NIO has a market cap of $71 billion, showing that investors are optimistic about expectations for electric vehicle intelligence.

The market cap revaluation of Chinese car companies is underway, with Great Wall Motors’ market cap reaching over RMB 300 billion as of June 21, 2021. Car companies including BAIC Bluepark and Sokon have also seen significant growth in market capitalization in the last two years along with the wave of automotive electric intelligence.

Prediction 7: Local Brand Hybrids to Replace Fuel Cars on a Large Scale

China’s double credit policy was officially released on September 28, 2017, and started to be implemented in April 2018.

It puts high requirements on the fuel consumption of traditional vehicles and the production of new energy vehicles. Low fuel consumption models with advanced electrification technology will enjoy the benefits of credit calculation and become beneficiaries.

Li Jun, Chairman of China-SAE, has said that hybrid passenger cars will account for more than 50 percent of traditional car sales by 2025. By 2035, all traditional energy-powered passenger cars will be replaced with hybrids, and new energy vehicles will become mainstream.

Geely is developing a new generation of hybrid powertrain, and the thermal efficiency of the hybrid-specific engine will exceed that of all products on sale in the market, with a target fuel saving rate of 45 percent.

SAIC announced the “3.0T Green Power” technology on September 23, 2020, and launched the first SUV with this technology, the Roewe RX5 ePLUS.

More than 10 models equipped with this technology will be launched in the next five years.

GAC Trumpchi is the first local brand to be equipped with Toyota’s hybrid powertrain THS, and GAC Group is also developing its own GMC hybrid system.

By the end of 2021, the first GAC Trumpchi flagship model with the Toyota THS dual-motor hybrid system will be available.

Prediction 8: Investors are more concerned about R&D, technology, FOTA

The most important components of new energy vehicles are motor, electric control, battery, and intelligent experience, and the amount of investment in R&D will directly affect the future of car companies.

The more car companies invest in R&D, the more patents and achievements they can obtain, which is also more conducive to their future sustainable development.

New car makers are choosing the pure electric route, and old traditional car companies are iterating engine technology while starting the electrification transformation.

In terms of sales concentration, the market share of the top 15 in China has reached 77.5 percent. Compared to 2019, the top 15 car companies in 2020 have also increased their sales share of the overall market by 3 percentage points.

Prediction 9: Investors look more at supply cycles driven by technological innovation

The auto market has entered a downward cycle since 2017 due to factors such as cost, product cycles, epidemics, and chip shortages.

China’s auto sales experienced more than a decade of rapid growth and peaked for the first time in 2017. 2017 to 2020, China’s narrow passenger car sales declined from 23,764,400 to 19,288,000.

Smart car penetration grows more than nine-fold in four years, from 5.2 percent in 2016 to 51.6 percent in 2020.

According to the 2019 Gartner Technology Maturity Curve, vehicles with Level 3 autonomous driving hardware capabilities will be widely produced.

Sensor technologies such as detection and ranging (Lidar), which are primarily used to enable autonomous driving, will be a popular component in the automotive industry over the next five years.

Autonomous driving levels 4 and 5 will be achieved with more sophisticated software and more powerful computing. Along with the continuous introduction of new technologies and models, the automotive industry will shift from being driven by consumer demand to being driven by technology product supply.

Prediction 10: Car company valuation methods need to switch from PB to PE

Profit will no longer be the only criterion to measure the success of startups. In the near term, low profits in 3-5 years will not be a factor that hinders their growth.

Teala has also been unprofitable for many years. From 2011 to date, Teala has only achieved its first annual profit for the first time in 2020, but its market capitalization has been much higher than that of traditional auto giants including Toyota and Ford.

The new car makers have not yet achieved profitability. The 2020 earnings reports of US-listed NIO, XPeng, and Li Auto show they are still in the red, with Li Auto losing RMB152 million, NIO losing RMB5.610 billion, and XPeng losing RMB2.732 billion.

As of June 26, 2021, Li Auto’s market capitalization is $28.7 billion, NIO’s is $68.8 billion, and XPeng’s is $35.7 billion, so profitability will no longer be the only measure of success.

The traditional auto stock valuation method is based on PE and PB. Traditional auto companies are more stable in production and profitability, so the traditional valuation PE and PB method is more applicable.

The new era of automotive stock valuation methods will be more diversified, and the future may be PS or more ways.

Profit is no longer the only criterion, sales revenue is more stable and less volatile, PS or more ways will gradually apply.

This article was first published by Phate Zhang on CnEVPost, a website focusing on new energy vehicle news from China.

{kind=link}