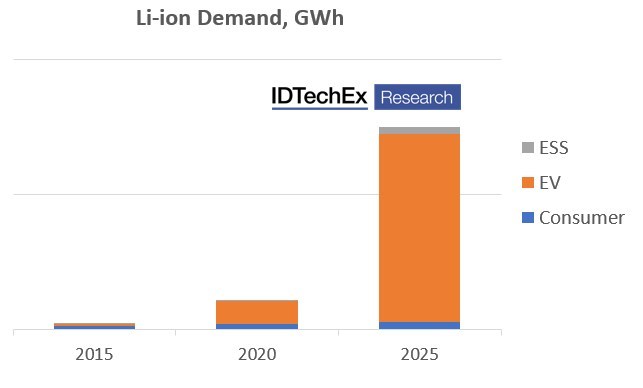

IDTechEx forecast the Li-ion market to grow to over US$430 billion by 2033, driven by demand for electric vehicles. Electric vehicles (EVs) remain the key driver behind the Li-ion market, and electric cars will be the largest market for Li-ion batteries over the next ten years. As a result of its growing importance, the EV market will be a key determinant of the Li-ion battery technologies used and developed. A key aspect of this are the cathode choices made by the Li-ion market.

The past ten years have seen the majority of the EV market outside China rely on NMC (nickel-manganese-cobalt oxide) and NCA (nickel-cobalt-aluminum oxide) cathodes due to their high energy density, which provides long EV ranges. Shifts in these cathode materials have come from increasing the nickel content and reducing the amount of cobalt used.

NMC 111 (equal parts Ni, Mn, Co) has been replaced by NMC 532 and NMC 622, the use of NMC 811 is expanding, and major cathode manufacturers are looking to move toward 90+% nickel in NMC and NCA. This is being driven by a desire to reduce expensive and potentially problematically sourced cobalt, as well as to increase capacity and energy density as much as possible. Difficulties remain in ensuring the safety and longevity of these materials.

While NMC and NCA cathodes will remain important, especially in Europe and North America, pressures seen on battery prices through 2021 and 2022, and the potential for future material supply disruptions, have forced EV makers and battery manufacturers to re-think strategies. Various automakers, including Tesla, Volkswagen, Ford, and Stellantis, amongst others, have outlined plans to make use of cheaper LFP (lithium iron phosphate) cathodes in some regions for mass-market or lower-cost vehicle segments.

LFP has already regained market share over the past two years due to its recapture of EV market share in China in particular. IDTechEx expects LFPs share of the total Li-ion market (by GWh) to increase over the next ten years. An indication of this can be seen through IDTechEx’s estimate of production capacity by cathode type, where LFP production capacity is expected to grow at a CAGR of ~31% over the next five years, while NMC and NCA production capacity is expected to grow at a CAGR of ~19%. This growth in LFP will be driven by pressure to reduce battery prices for both electric vehicles and stationary battery storage systems.

While LFP is already well suited for stationary applications, for an electric vehicle, where energy density remains a key performance metric, technological innovations could help minimize the impact of its lower energy density compared to NMC/NCA and make LFP an even more attractive proposition. These improvements could stem from the use of silicon anodes, cell-to-pack designs, or other drivetrain efficiency gains.

However, a push to limit reliance on cobalt and nickel by shifting to LFP will increase reliance on China, as the vast majority of LFP production is coming from Chinese companies (in China) with relatively few plans for LFP production outside the country. This would be contrary to the aims and objectives of governments and players in Europe and North America.

More recently, high manganese cathodes have garnered attention, with EcoPro BM and Umicore joining BASF in outlining their intention to commercialize high manganese cathodes. Development of these cathodes is also driven by a desire to reduce costs, while they also benefit from allowing comparable energy density to NMC/NCA. Voltage fade and low cycle life remain key barriers to adoption.

LNMO is another interesting cathode development that could offer high-rate capability, comparatively low costs, and opportunities for improving the efficiency of battery pack designs. It could also reduce lithium consumption by having a lower kg/kWh lithium intensity compared to other cathodes, which could become highly important if supply constraints materialize and manufacturers are forced to find ways to minimize the impact of high lithium prices. Like the high-manganese cathodes above, cycle life, as well as the need for a stable electrolyte, remain key barriers.

{kind=link}