In the face of adversities within the autonomous vehicle market, car manufacturers are not hitting the brakes. Rather, they’re zeroing in, adopting more focused and streamlined strategies, deeply rooted in core technologies.

Eager to expedite the mass-scale rollout of Robotaxis, Tesla recently announced an acceleration in the development of their Dojo supercomputer. They are now committing an investment of $1 billion and set to have 100,000 NVIDIA A100 GPUs ready by early 2024, potentially placing them among the top five global computing powerhouses.

While Tesla already boasts a supercomputer built on NVIDIA GPUs, they’re still passionate about crafting a highly efficient one in-house. This move signifies that computational capability is becoming an essential arsenal for automakers, reflecting the importance of mastering R&D in this regard.

HPC Fosters Collaboration in the Car Ecosystem

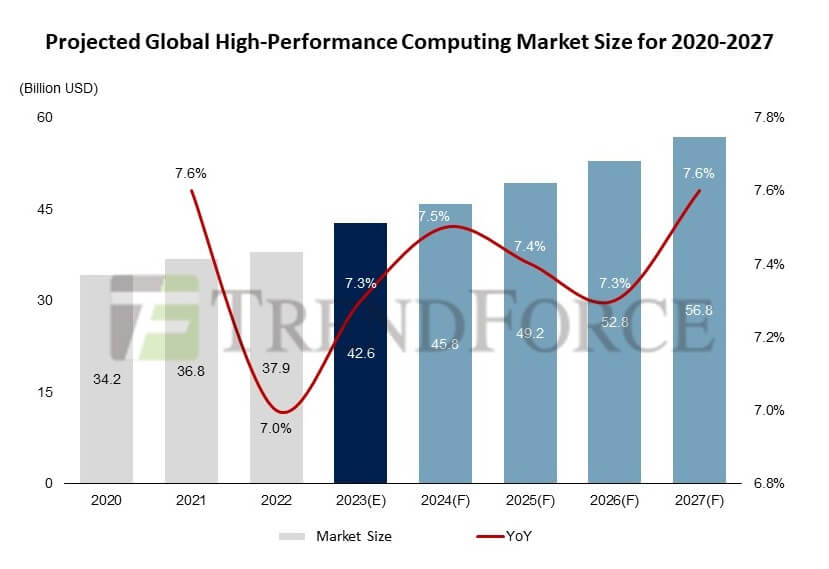

According to forecasts from TrendForce, the global high-performance computing(HPC) market could touch $42.6 billion by 2023, further expanding to $56.8 billion by 2027 with an annual growth rate of over 7%. And it is highly believed that the automotive sector is anticipated to be the primary force propelling this growth.

Feeling the heat of industry upgrades, major automakers like BMW, Continental, General Motors, and Toyota aren’t just investing in high-performance computing systems; they’re also forging deep ties with ecosystem partners, enhancing cloud, edge, chip design, and manufacturing technologies.

For example, BMW, who’s currently joining forces with EcoDataCenter, is currently seeking to extend its high-performance computing footprint, aiming to elevate their autonomous driving and driver-assist systems.

On another front, Continental, the leading tier-1 supplier, is betting on its cross-domain integration and scalable CAEdge (Car Edge framework). Set to debut in the first half of 2023, this solution for smart cockpits offers automakers a much more flexible development environment.

In-house Tech Driving Towards Level 3 and Beyond

To successfully roll out autonomous driving on a grand scale, three pillars are paramount: extensive real-world data, neural network training, and in-vehicle hardware/software. None can be overlooked, thereby prompting many automakers and Tier 1 enterprises to double down on their tech blueprints.

Tesla has already made significant strides in various related products. Beyond their supercomputer plan, their repertoire includes the D1 chip, Full Self-Driving (FSD) computation, multi-camera neural networks, and automated tagging, with inter-platform data serving as the backbone for their supercomputer’s operations.

In a similar vein, General Motors’ subsidiary, Cruise, while being mindful of cost considerations, is gradually phasing out NVIDIA GPUs, opting instead to develop custom ASIC chips to power its vehicles.

Another front-runner, Valeo, unveiled their Scala 3 in the first half of 2023, nudging LiDAR technology closer to Level 3, and laying a foundation for robotaxi(Level 4) deployment.

All this paints a picture – even with a subdued auto market, car manufacturers’ commitment to autonomous tech R&D hasn’t waned. In the long run, those who steadfastly stick to their tech strategies and nimbly adjust to market fluctuations are poised to lead the next market resurgence, becoming beacons in the industry.

For more information on reports and market data from TrendForce’s Department of Semiconductor Research, please click here, or email Ms. Latte Chung from the Sales Department at [email protected]

{kind=link}