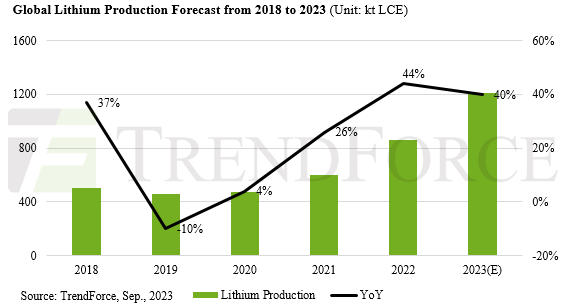

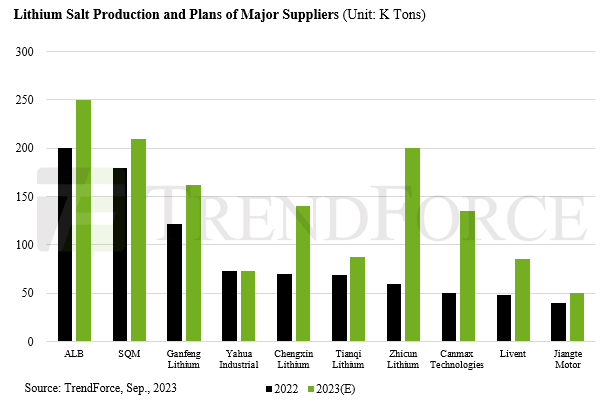

Australian mining company, Liontown Resources Ltd., has just announced it’s agreed to a buyout proposal of AUD 6.6 billion (USD 4.3 billion) by US lithium producer Albemarle Corp (ALB). TrendForce’s latest “2023 Global Li-Ion Battery Industry Chain Market Supply and Demand Report,” indicates that global lithium production in 2022 hit approximately 860,000 tons of Lithium Carbonate Equivalent (LCE). ALB, with its diverse lithium portfolio (spodumene, lithium salt, and tolling), accounted for over 180,000 tons of LCE. Predictions for 2023 spotlight a global lithium production reaching 1.21 million tons LCE, and ALB is set to churn out 200,000 tons of that, holding firmly onto the lead with its 17% market share.

TrendForce reports that ALB has strategically secured the planet’s most abundant, high-quality, and cost-efficient reserves of lithium salt lake and minerals across regions like Chile, Australia, and the US. Moreover, when it comes to lithium refinement, ALB emerges as the global titan with the world’s greatest lithium salt production capacity. As it stands, ALB’s annual production capacity for lithium hydroxide reaches 110,000 tons, accounting for 23% of the world’s entire production.

With ambitions to acquire Australian miner Liontown, ALB set to command the world’s largest lithium resources

Liontown, a key supplier of Australia’s battery minerals, holds the reins to two major hard rock lithium deposits: Kathleen Valley and Buldania. These areas boast lithium reserves of 156 million tons (5.4 million tons LCE) and 14.9 million tons (370,000 tons LCE), respectively. As Kathleen Valley gears up for completion by the end of 2023, its inaugural production phase is set to roll out by 2Q24, targeting an annual yield of 500,000 tons of lithium spodumene concentrate. And that’s just the start, with plans to elevate this figure to a whopping 700,000 tons annually. On the other hand, the Buldania project is still in its nascent stage, focused on exploration and surveying.

Should ALB’s acquisition of Liontown materialize, it would cement its control of global lithium resources and bolster its lithium salt production framework. Yet, ALB isn’t the sole player in this vast industry. Major lithium producers, including SQM, Tianqi Lithium, Ganfeng Lithium, Yahua Industrial, Chengxin Lithium, and Livent, are fervently ramping up their production capabilities in lithium carbonate and lithium hydroxide.

Lithium, the backbone of modern tech, is set to see its global demand skyrocket. TrendForce’s insights reveal a bustling 2022 with around 40 lithium mining projects worldwide. After 2025, the number of projects in production will increase to a staggering 100+. To safeguard their global dominance and sharpen their competitive edge, lithium chemical producers are strategically aligning with upstream lithium miners to secure lithium resources. Case in point: Livent’s recent merger with Allkem in May of this year and ALB’s designs on Liontown. This momentum signifies a trend toward a more consolidated global lithium resource landscape, with mergers and acquisitions becoming the norm in upcoming years.

{kind=link}