Hybrid Research: China Hybrid EV penetration rate will hit 22% within five years

With the development of automobile energy-saving and new energy technologies and the promotion of low-carbon emission reduction policies worldwide, fuel economy and low-carbon emissions have been in the spotlight of automobile development, and hybrid electric vehicles have become R&D focus of current automobile industry.

The commercialization of hybrid vehicles has been developing for more than 20 years, with four major markets in the world: Europe, the United States, Japan, and China, which differ in technology, strategy and marketplace. Different automakers are also diversifying their hybrid system architectures. At present, hybrid technologies vary with technology platforms.

Hybrid vehicles are accelerating the pace of replacing fuel vehicles in China

According to statistics, 6.495 million new energy passenger cars (EVs+PHEVs) were sold globally in 2021, up 107.9% year-on-year with the market share hitting a record as high as 9%; wherein, the sales volume of battery-electric passenger cars (EVs) swelled by 69% year-on-year to 4.6 million units, and the sales volume of plug-in hybrid electric passenger cars (PHEVs) increased by 31% year-on-year to approximately 1.9 million units. In 2021, the global sales volume of energy-efficient HEVs jumped by more than 20% year-on-year to approximately 3.5 million units.

Catalyzed by a series of policies such as emission regulations, Measures for the Parallel Management of Corporate Average Fuel Consumption (CAFC) and New Energy Vehicle (NEV) Credits of Passenger Car Companies, Energy-saving and New Energy Vehicle Technology Roadmap 2.0, energy-saving and new energy vehicles are burgeoning. Low fuel consumption and Measures for the Parallel Management of Corporate Average Fuel Consumption (CAFC) and New Energy Vehicle (NEV) Credits of Passenger Car Companies have prompted automakers to accelerate the transformation toward electrification and speed up the deployment of 48V, HEV, REEV, PHEV and other hybrid roadmaps.

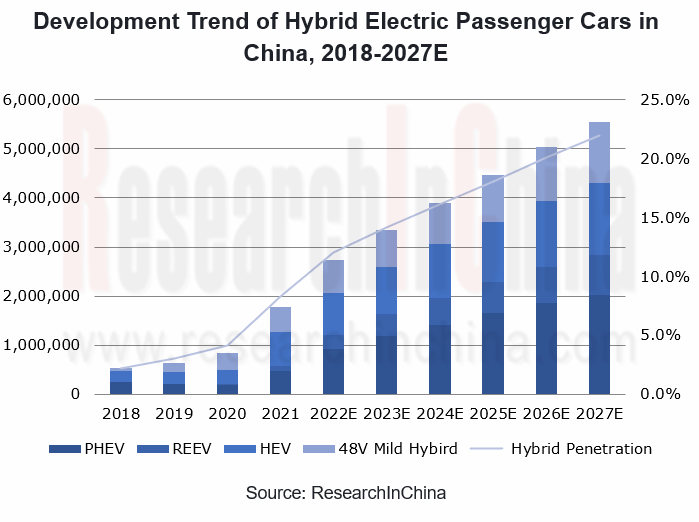

In 2021, the sales volume of hybrid passenger cars in China reached 1.778 million units, including 470,000 PHEVs, 105,000 REEVs, 689,000 HEVs, and 513,000 48V mild hybrids. With the development of hybrid systems of Chinese independent brands, PHEVs will outsell HEVs and 48V mild hybrids by 2022. REEVs have performed well since the launch, and will still grow at a relatively high growth rate from 2022 to 2027.

The penetration rate of hybrid electric passenger cars in China will fetched 8.3% in 2021, and it is expected to hit 22% by 2027 with sales over 5.5 million units.

After several years of development, Chinese independent brand automakers have made significant progress in hybrid vehicle technology, even surpassed Japanese companies such as Toyota and Honda in some aspects of performance. Their models cover weak hybrids, mild hybrids/medium hybrids, strong hybrids and so on:

Micro Hybrid – Start / Stop (12V): The currently available start / stop 12V passenger car models mainly come from European and American brands, while Chinese independent brands account for 19% of the total models;

Mild/Medium Hybrid (48V): Although Chinese independent brand automakers have deployed 48V mild hybrid system technology, they offer few models, and almost only FAW-Hongqi, Geely and Great Wall have sold cars equipped with the technology.

PHEV: BYD DM, DM-i, Great Wall L.E.M.O.N DHT, Geely Thor Hybrid Hi·X, Changan Blue Whale iDD and other hybrid systems have been mass-produced. BYD DM and DM-i have been installed on many of its models; DHT, has been applied to Mocha, Latte, Macchiato and other models of Great Wall; Changan Blue Whale iDD has been applied to UNI-K, UNI-V models;

REEV: The REEVs currently for sale mainly include Seres SF5, AITO M5, Li ONE and Voyah FREE. In June 2022, Li Auto released a full-size SUV – Li L9, and AITO unveiled a medium and large range-extended SUV – AITO M7. Both were so appealing that they received over 20,000 orders upon launch.

OEMs have mass-produced a new generation of DHE + DHT + integrated electric drive hybrid architecture

From the perspective of technical route selection:

48V hybrid technology maintains steady growth by continuously improving motor efficiency and electrification level. At this stage, it is mainly driven by foreign OEMs;

HEV technology-based models pay more attention to development of energy saving, cost reduction, system simplification, etc.;

PHEV technology is developing towards low energy consumption and high cost performance, and China has explored an independent development of PHEV technology path;

REEV technology is complementary to other hybrid technologies due to its simple structure. High battery life and driving experience are welcomed by consumers. Driven by star models such as Li, AITO, and Voyah, it will grow rapidly in the next few years.

From the perspective of hybrid technology platform layout of OEMs, domestic OEMs have independently developed DHE (hybrid special engine) + DHT (hybrid special transmission assembly), and the platform supports multiple hybrid architectures such as HEV, PHEV, and REEV at the same time:

{kind=link}