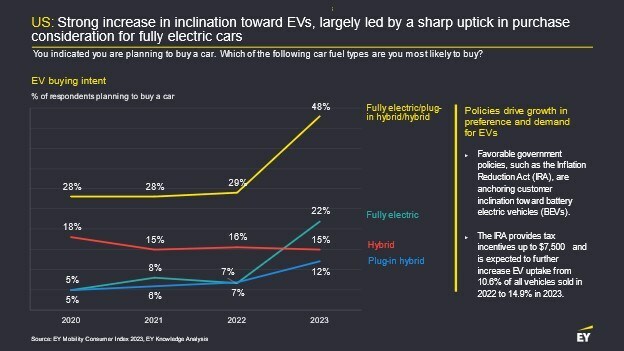

The latest EY Mobility Consumer Index (MCI) — a global EY survey of more than 15,000 consumers from 20 countries — reveals that US consumer interest in electric vehicles (EVs) is at an all-time high, with about half (48%) of US car buyers intending to purchase an EV in the next 24 months. This represents a 19% increase since the 2022 MCI findings, showing the highest growth in EV intent and sentiment, globally. In EV readiness overall, the US jumped five spots, reaching No. 7, falling behind China, Norway and Sweden in the top three spots.

Shifting mobility behavior drives sharp increase in demand

In 2023, the share of existing car owners intending to buy new cars in the US showed a 3% increase, with the US showing a significantly higher car-buying intent (12% growth to 60%) compared with the global average (which remained flat year over year at 44%).

The rise of the electric SUV — or SU(E)V — continues to prove strong, with 38% of North American buyers preferring an SUV over a sedan or other vehicle type. Further, 40% of new car buyers and 37% of used car buyers would prefer purchasing an SUV over other car body types. This promise of consumer interest should embolden car companies to invest in EV models for larger vehicles.

Consumer confidence gains momentum, but doubts about EV infrastructure and safety remain

Consumer confidence in EV performance has steadily grown over the past two years. In 2021, MCI findings noted that 26% of US car buyers were concerned that internal combustion engine (ICE) vehicles outperformed EVs. Today, in comparison with ICE vehicles, EV performance was the top motivation for buying an EV, with 29% of US car buyers considering an EV specifically because they believe it outperforms ICEs.

“There are a few critical drivers to adopt EVs on a large scale, from consumer sentiment, to regulatory incentives and cost,” said Felipe Smolka, EY Americas Automotive eMobility Leader. “Government incentives, such as the Inflation Reduction Act (IRA), make a large impact not just on consumers, but across industries. As more EV accessibility and incentives arise, whether its developing charging stations on interstate highways or driving battery circularity, we will see EV adoption thrive.”

Clear gains in the market are tempered by ongoing concerns about EV charging infrastructure, costs and safety. A lack of charging stations continued to be the top deterrent for potential car buyers in the US, the same as 2022. Over half (51%) of US consumers are more worried about finding a charging station in nonresidential facilities than expensive charging costs. Further, the safety of home chargers remains a concern, with 57% of potential US buyers citing safety of home chargers as the key deterrent — 10% higher than global counterparts.

“Consumers need access to safe, reliable, convenient and affordable charging to drive and own an EV, and our research shows real concerns remain,” said Marc Coltelli, EY Americas eMobility Energy Leader. “At the EY organization, we are predicting 82 million EVs will be on US roads by 2035. To scale adoption, the challenge confronting America’s transition to EVs is instilling charging confidence among consumers. The energy industry has a massive role to play in this transition and is seizing the opportunity by collaborating cross-sector to build and power a resilient EV charging network.”

As the infrastructure, performance, circularity, life-span and financial value of an EV increases in the US market, we can expect to see continued adoption of EVs, both in commercial and consumer applications.

{kind=link}