TrendForce’s latest “2Q26 Global Solid-State Battery Industry Development Quarterly Report” reveals that the Japanese government has significantly expanded support for next-generation battery technologies in recent years.

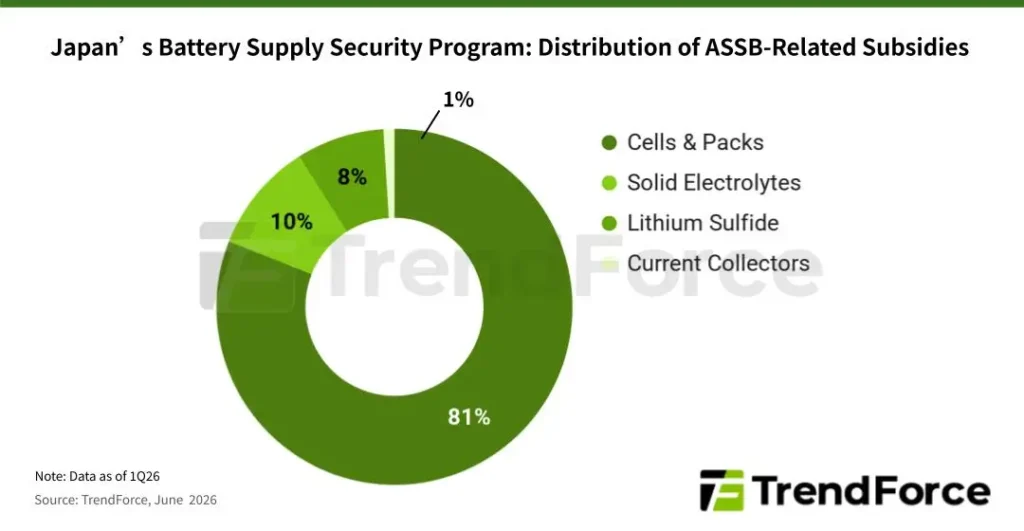

Since 2023, Japan’s Ministry of Economy, Trade and Industry (METI) has been implementing the Battery Stable Supply Assurance Plan, which prioritizes the development and early-stage commercialization of technologies such as all-solid-state batteries (ASSBs) and bipolar low-cost lithium iron phosphate (LFP) batteries. As of the first quarter of 2026, the program has approved five major projects related to the ASSB supply chain, with total subsidies reaching $660 million (¥105.7 billion).

TrendForce notes that ASSBs offer significant performance advantages over conventional liquid lithium-ion batteries and are now progressing from laboratory research toward engineering validation and commercial preparation. Beyond Japan, countries including South Korea, China, and the United States have also designated solid-state batteries (SSBs) as a strategic technology priority.

Japan aims to commercialize ASSBs around 2030. Major automakers including Toyota, Honda, and Nissan have already established pilot production lines for ASSBs. With commercialization roadmaps becoming increasingly defined, the industry’s primary objectives in 2026 are to improve battery yield and quality while expanding production capacity for critical materials to reduce costs—particularly sulfide solid electrolytes and lithium sulfide (Li₂S).

TrendForce estimates that approximately 18% of METI’s approved ASSB-related funding has been allocated to the development and optimization of production technologies for solid electrolytes and lithium sulfide.

TrendForce points out that Japan currently remains the world’s leading source of ASSB technology. Japanese companies account for approximately 37% of global SSB patent filings, while the country continues to accelerate supply-chain development to secure future market share and maintain industrial competitiveness.

However, Japan’s strategy of leveraging ASSBs as a competitive advantage faces several challenges. Chief among them is the rapid advancement of low-cost LFP batteries led by Chinese manufacturers, as well as intensifying global competition in next-generation battery technologies.

The share of LFP batteries in EVs continues to rise, supported by leading manufacturers such as CATL and BYD. These companies have successfully reduced battery costs while improving performance through innovations such as Cell-to-Pack (CTP) architecture and ultra-fast charging technologies. As a result, LFP batteries present a significant cost barrier to the adoption of ASSBs in the automotive market.

China, South Korea, Europe, and the United States are making significant investments in SSB development. South Korea’s Samsung SDI is progressing toward commercialization, matching the timeline of Japanese rivals.

Furthermore, Chinese firms are adopting a dual strategy: securing an early market share with semi-solid-state batteries and boosting investments in ASSB tech. China is enhancing collaboration across materials, equipment, battery cells, and automotive sectors to tackle the remaining challenges of mass production for ASSBs.

{kind=link}